Beneath today’s elevated stock prices lies a complex web of hidden leverage embedded in margin debt, options markets, corporate buybacks, private credit, and liquidity mismatches. While markets appear stable on the surface, this concealed leverage amplifies downside risk and increases the likelihood of sudden market shocks. Understanding where leverage hides is now essential for modern investors.

Introduction: Why Today’s Stock Market Feels Strong—but Unsettling

The U.S. stock market appears confident. Indexes sit near record highs, volatility remains subdued, and many headlines emphasize economic resilience. To casual observers, this looks like a healthy market digesting higher interest rates and global uncertainty with ease.

Yet for experienced investors, something feels off.

This discomfort isn’t driven by inflation headlines or Federal Reserve policy alone. Instead, it stems from a deeper concern—one that rarely dominates financial news until it’s too late. That concern is hidden leverage.

History shows that markets rarely collapse simply because valuations are stretched. They break when leverage amplifies small shocks into systemic events. The danger today is not that leverage is obvious—it’s that much of it is concealed beneath the surface, embedded in financial structures most investors rarely examine.

From options markets and corporate balance sheets to private credit and ETF mechanics, leverage has not disappeared since past crises. It has evolved, dispersed, and become harder to track. Understanding this hidden leverage may be the most important investment skill of the next decade.

What Is Hidden Leverage, and Why Does It Matter?

Hidden leverage refers to financial exposure that magnifies gains and losses without being clearly visible in traditional market indicators such as price-to-earnings ratios, index levels, or headline debt figures.

Unlike classic leverage—borrowing money to buy stocks—hidden leverage operates quietly through:

- Derivatives and options

- Balance-sheet engineering

- Liquidity mismatches

- Off-balance-sheet financing

- Non-bank lending structures

This makes it especially dangerous. When leverage is hidden, risk appears manageable until it suddenly isn’t.

In calm markets, hidden leverage boosts returns and reinforces confidence. But when prices stall or decline, the same leverage forces selling, drains liquidity, and accelerates losses. By the time investors recognize the problem, the damage is often already done.

Why Hidden Leverage Has Grown Over the Past Decade

To understand today’s market fragility, it helps to revisit what changed after the 2008 financial crisis.

Following the collapse:

- Banks faced stricter capital requirements

- Traditional lending became more conservative

- Regulators focused heavily on visible systemic risk

But financial markets do not eliminate risk—they relocate it.

Years of low interest rates encouraged investors to chase yield. Institutional capital flowed into new vehicles promising higher returns with “controlled” risk. Innovation flourished, but so did complexity.

As a result, leverage migrated away from traditional banks into:

- Hedge funds and asset managers

- Options and derivatives markets

- Private credit funds

- Corporate balance sheets

The system became less transparent, not less leveraged.

Where Hidden Leverage Is Lurking Today

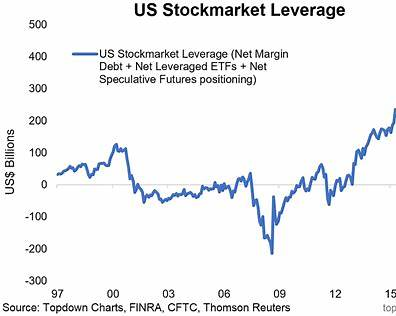

Margin Debt: Familiar Risk, Larger Impact

Margin debt—money borrowed by investors to buy stocks—has repeatedly reached historically elevated levels over the past decade. While it rises and falls with markets, its structural role has grown.

Margin works smoothly on the way up. Gains are amplified, reinforcing optimism. But on the way down, margin becomes ruthless.

When stock prices fall:

- Brokers demand additional collateral

- Investors are forced to sell

- Selling pressure accelerates declines

Real-life example:

In March 2020, forced deleveraging was a major driver of the market’s historic collapse. Investors didn’t sell because they wanted to—they sold because they had to.

Options Markets: Leverage Without Borrowing

Options trading has surged among both retail and institutional investors. While options don’t look like traditional leverage, they effectively allow investors to control large exposures with relatively small amounts of capital.

This dynamic can distort price behavior.

As stocks rise:

- Call option buying increases

- Market makers hedge by buying shares

- Share prices rise further

- The cycle feeds on itself

When sentiment shifts, this process can reverse violently, leading to sharp and sudden declines.

Options leverage often remains invisible in market narratives, yet it plays a powerful role in amplifying short-term volatility.

Corporate Buybacks and Balance-Sheet Leverage

Stock buybacks have become a dominant force in equity markets. By reducing share counts, buybacks boost earnings per share and support stock prices.

However, many buybacks are funded with borrowed money.

This creates a subtle but important form of leverage:

- Corporate debt increases

- Financial flexibility declines

- Balance sheets become more fragile

During economic slowdowns, buybacks are often the first thing to disappear—removing a major source of demand just when markets need it most.

Historical reminder:

In 2020, corporate buybacks collapsed almost overnight, contributing to market instability at the worst possible moment.

Private Credit: The Quiet Growth Engine of Leverage

One of the least understood sources of hidden leverage today is private credit—loans issued outside the traditional banking system by private equity firms and asset managers.

Private credit has grown rapidly because:

- It offers higher yields

- It faces lighter regulation

- Institutional investors crave income

But transparency is limited.

Many borrowers are already highly leveraged. Loan terms are complex, and pricing is often opaque. Because these assets don’t trade publicly, risk can remain hidden until defaults rise sharply.

This makes private credit a potential shock amplifier during economic stress.

ETFs and Liquidity Mismatch

ETFs promise instant liquidity, but not all the assets they hold can be sold quickly.

This mismatch becomes dangerous during market stress:

- Investors sell ETF shares instantly

- Underlying assets struggle to find buyers

- Prices disconnect from fundamentals

Bond ETFs and niche equity ETFs have already shown signs of this strain during periods of volatility, raising concerns about broader contagion risks.

Why Markets Keep Underestimating Leverage Risk

Hidden leverage thrives because markets are conditioned to believe in stability.

Several forces reinforce this mindset:

- Long periods of low volatility

- Repeated central bank interventions

- Rapid recoveries from past sell-offs

This creates complacency. Investors come to expect that shocks will be short-lived and manageable. But leverage doesn’t respond to confidence—it responds to price movement and liquidity.

When leverage unwinds, it does so mechanically, not emotionally.

What Happens When Hidden Leverage Unwinds?

Leverage unwinding rarely unfolds slowly. It usually follows a familiar pattern:

- A modest shock disrupts expectations

- Prices move unexpectedly

- Leverage forces selling

- Liquidity dries up

- Losses cascade across markets

Importantly, the initial trigger doesn’t need to be dramatic. It could be:

- Slightly weaker earnings

- A rise in bond yields

- A regulatory change

- A geopolitical development

Leverage determines the severity, not the trigger.

How Investors Can Reduce Exposure to Hidden Leverage

While no investor can eliminate risk entirely, awareness goes a long way.

Practical steps many investors are taking include:

- Favoring companies with strong balance sheets

- Avoiding excessive margin use

- Understanding options exposure, even indirectly

- Maintaining liquidity for volatile periods

- Diversifying across asset classes, not just sectors

Risk management is not about predicting crashes—it’s about surviving them.

Key Takeaways

- Hidden leverage magnifies losses when markets turn

- Options, buybacks, private credit, and ETFs embed leverage

- Calm markets often mask the greatest fragility

- Leverage doesn’t cause downturns—it amplifies them

- Awareness and discipline are critical investor advantages

Frequently Asked Questions (Trending Search Queries)

1. What is hidden leverage in the stock market?

Hidden leverage refers to financial exposure that amplifies risk without appearing in standard valuation or debt metrics, such as derivatives, margin debt, and balance-sheet strategies.

2. Why is hidden leverage dangerous?

Because it masks true risk levels and accelerates losses when markets decline, often triggering forced selling and liquidity crises.

3. Is margin debt a warning sign for markets?

High margin debt can increase vulnerability to sharp sell-offs, especially when prices begin to fall unexpectedly.

4. How do options increase market volatility?

Options allow large exposures with little capital, creating feedback loops that magnify both gains and losses.

5. Are corporate buybacks risky for investors?

Buybacks funded by debt can weaken balance sheets and reduce corporate resilience during downturns.

6. What role does private credit play in market risk?

Private credit adds leverage outside regulated banking systems, increasing opacity and systemic vulnerability.

7. Can ETFs worsen market crashes?

Yes. Liquidity mismatches in ETFs can amplify volatility during periods of stress.

8. Is today’s leverage worse than in 2008?

Leverage today is less concentrated but more dispersed and harder to track, making it potentially more unpredictable.

9. How can investors spot leverage risk early?

Rising volatility, widening credit spreads, sudden price gaps, and declining liquidity are common warning signs.

10. Should long-term investors worry about leverage?

Yes. Leverage increases drawdowns and recovery times, even for diversified portfolios.

Final Thoughts: The Risk You Don’t See Is the One That Hurts Most

Markets rarely collapse under the weight of fear alone. They collapse under the weight of leverage that was ignored during good times.

Hidden leverage doesn’t mean disaster is imminent. But it does mean the margin for error is thinner than it appears. For investors navigating today’s markets, understanding where leverage hides may be the most valuable form of protection available.